Blockchain technology has been proposed to power financial products, to provide cybersecurity solutions and even to enable people to sell their homes without a real estate agent. In fact, this distributed ledger technology has been seen as a solution for a wide range of real world challenges. But the question for entrepreneurs remains whether if this technology is actually beneficial for their business. To answer that, Deutsche Bank Chief Data Officer JP Rangaswami and other colleagues at the World Economic Forum have developed an exhaustive guide to help entrepreneurs that are asking themselves that exact same question.

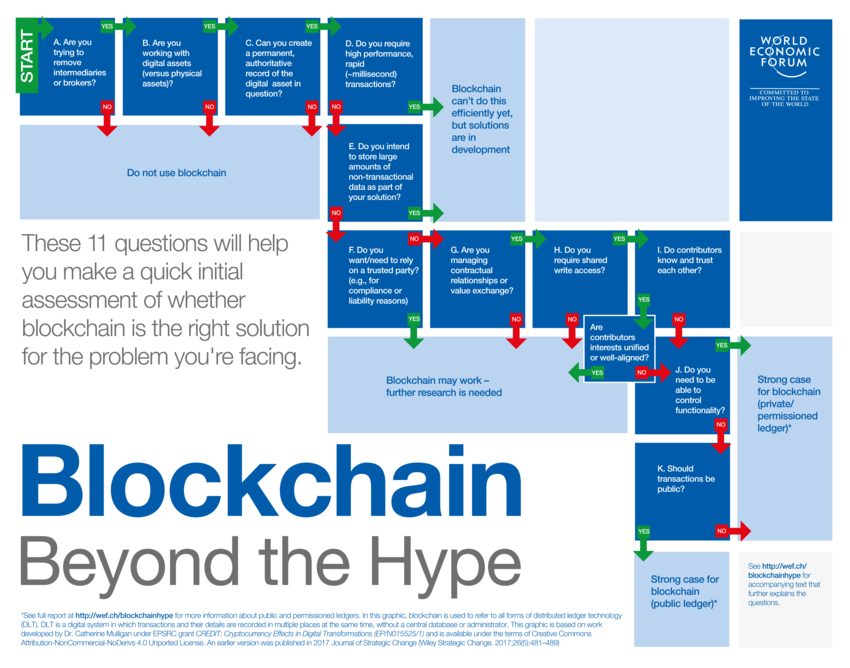

Research by Gartner shows that by 2023, blockchain will support the global movement and tracking of $2 trillion of goods and services annually. That is why is so important right now to understand if blockchain is right for a business or not. This guide is a 11-question document that most entrepreneurs should ask themselves before going all-out with blockchain technology and it is based on an analysis of how blockchain is used in a variety of projects around the world and following interviews with selected chief executive officers.

“These 11 questions were developed and then trialled with chief executive officers at a workshop at the World Economic Forum Annual Meeting 2018. The test group included C-suite executives from large corporations, most of whom said they were actively considering adopting blockchain technology in some manner,” Deutsche Bank Chief Data Officer JP Rangaswami said.

The 11 question guide:

- Are you trying to remove intermediaries or brokers?

- Are you working with digital assets (versus physical assets)?

- Can you create a permanent, authoritative record of the digital asset in question?

- Do you require high performance, rapid (millisecond) transactions?

- Do you intend to store large amounts of non-transactional data as part of your solution?

- Do you want/need to rely on a trusted party (e.g., for compliance or liability reasons)?

- Are you managing contractual relationships or value exchange?

- Do you require shared write access?

- Do contributors know and trust each other?

- Are contributors interests unified or well-aligned?

- Do you need to be able to control functionality?

- Should transactions be public?

The paths were incorporated into a framework of “yes” and “no” questions, which guide a business leader once a specific problem is articulated. “This framework cuts through the noise about blockchain and refocuses the technology into the way business leaders think,” said Jennifer Zhu Scott, Founding Partner of Radian and member of the Global Futures Council on Blockchain.

Blockchain applications go beyond cryptocurrency and it is now being implemented in all sorts of businesses and industries. It is a computer technology that allows its participants to store and share data securely within the network. “Blocks” store the pieces of information, including the date, ID of transaction, time and even IDs of who is participating in that data transaction and in the whole of the blockchain. These blocks store information that distinguishes them from other blocks called “hash” that allows participants to tell it apart from every other block within the “chain.”